Automation Playbooks

Capital Goods and ITC Rules: Everything You Need to Know

A thorough overview of the ITC rules, calculations, and compliance requirements specifically related to claiming ITC on capital goods under GST.

Capital goods can lead to great savings—if you know how to claim the appropriate ITC under GST.

The Goods and Services Tax (GST) system has transformed taxation in India by introducing the Input Tax Credit (ITC) mechanism, which ensures tax is levied only on the value added at each stage. For businesses investing in capital goods, understanding the ITC rules—especially how the Input Tax Credit on capital goods ledger is created under GST provisions, is crucial to optimizing tax benefits and maintaining compliance.

In this blog, you will get a thorough overview of the ITC rules, calculations, and compliance requirements specifically related to claiming ITC on capital goods under GST.

Understanding ITC on Capital Goods under GST

Input Tax Credit refers to the credit, businesses can claim for the tax paid on purchases used in their operations. ITC helps businesses avoid the cascading effect of taxes, thereby reducing their overall tax liability and enhancing profitability.

As per Rule 40, clauses (c) and (d) of section 18 of the CGST Act, businesses must claim ITC on capital goods after reducing the tax paid by five percentage points for each quarter or part thereof, starting from the date of the invoice or any other relevant documents on which they received the capital goods.

Calculation of ITC for Capital Goods

Businesses generally distribute the ITC for capital goods over a specified period of five years. For mixed-use capital goods, where the asset serves both taxable and non-business purposes, Input Tax Credit calculation can be done using the following formula:

Credit=(ITC5)×12

Where:

ITC: Refers to the total ITC available for the capital goods.

5: Represents the number of years over which the credit is allocated (this may vary based on local tax regulations).

12: Signifies the number of months in a year.

This formula determines how businesses calculate the ITC for the initial 12 months of the asset’s lifespan. If businesses use capital goods for both business and non-business purposes, they must adjust the ITC based on the proportion of business use. Furthermore, if businesses use the capital goods to produce exempt supplies, they must make additional adjustments to ensure they don’t claim ITC for the portion of the asset’s use related to exempt supplies.

With these basic key concepts and ITC calculations in place, businesses can now uncover the eligibility criteria for claiming ITC on capital goods, helping them understand how they can benefit from tax credits on significant investments used in their operations.

Read more: Calculating Input Tax Credit (ITC) under GST: A Simple Guide

Eligibility to Claim ITC on Capital Goods

In India, the eligibility for claiming ITC for capital goods under the GST regime depends on several factors. Section 18 of the CGST Act specifies the conditions that GST-registered buyers must fulfill to claim ITC. Below are the key eligibility requirements:

The claimant must be a registered taxpayer under GST. An unregistered individual or business cannot claim ITC.

The capital goods must be used for business purposes, such as machinery, office equipment, or vehicles employed in business operations. ITC does not apply to personal use or exempt supplies.

Taxpayers must pay GST on the capital goods at the time of purchase, and they must possess a valid tax invoice. Proper documentation of these invoices is crucial for availing ITC.

Businesses should use capital goods for producing taxable goods or services or for providing taxable services. They cannot claim ITC for goods used in exempt supplies or for non-business purposes.

Businesses making both taxable and exempt supplies must apportion ITC based on their taxable turnover. They can claim ITC only for capital goods used in taxable supplies.

Once the eligibility criteria for ITC on capital goods are understood, businesses can proceed to examine the necessary documentation required for making ITC claims, ensuring full compliance with GST regulations.

Documentation Required for ITC Claims on Capital Goods

To claim ITC on capital goods under the GST regime, businesses must maintain specific documents that validate the claim. Below are the key documents businesses need to ensure compliance with GST regulations:

Tax Invoice or Debit Note: The supplier must issue a valid tax invoice or debit note that reflects the GST charged on the capital goods purchased.

Payment Receipt: The business must provide proof of payment, such as a bank transfer or cheque, to verify the transaction.

GST Compliance Records – GST registration number on the invoice, accurate entries in books of accounts, and reporting in GST returns (GSTR-1 and GSTR-3B).

Depreciation Details: Maintain details of depreciation claimed on capital goods as per the Income Tax Act, if applicable.

Additional Supporting Documents – Depending on the nature of capital goods, a manufacturer’s certificate, bill of supply, or purchase order may be required.

Once these documents are properly managed, the next critical step is to establish and maintain an accurate ITC ledger, which will track the utilization of tax credits, ensuring compliance and helping optimize GST benefits.

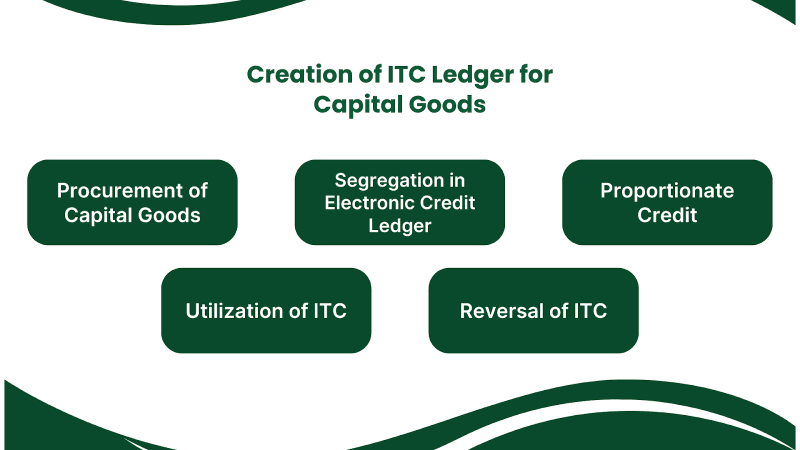

Creation of ITC Ledger for Capital Goods

Maintaining an accurate and up-to-date ITC ledger for capital goods is crucial for optimizing tax credits, avoiding penalties, and ensuring smooth compliance with GST regulations.

Procurement of Capital Goods: The GST paid on eligible capital goods is credited to the taxpayer’s electronic credit ledger under the “Capital Goods” category, ensuring proper tracking for future utilization.

Segregation in Electronic Credit Ledger: The electronic credit ledger records ITC under three categories: Inputs, Input Services, and Capital Goods. ITC on capital goods is separately recorded and utilized to offset GST liabilities.

Proportionate Credit: If capital goods are used for both taxable and exempt supplies, ITC is calculated proportionately. The reversal of ITC for exempt supplies is governed by Rule 43 of the CGST Rules and is performed monthly.

Utilization of ITC: ITC on capital goods can be used to pay GST on sales, as long as the required conditions are met. In most cases, you can use the full ITC unless there are specific rules that limit it.

Reversal of ITC: If capital goods are sold within five years of purchase, a proportionate reversal of the ITC claimed is mandatory, as per Section 18(6) of the CGST Act.

To better understand the challenges of managing the ITC ledger for capital goods, it’s important to explore how the utilization of capital goods can influence tax obligations, particularly when these assets are used for business versus non-business purposes.

Impact of Using Capital Goods: Business Vs. Non-Business Purposes

The utilization of capital goods for business versus non-business purposes can have significant implications on tax deductions, liabilities and credits. Below is an outline of the potential effects:

Use of Capital Goods for Business Purposes

Capital goods used for business purposes offer significant tax benefits, including depreciation deductions that reduce taxable income. Businesses can also claim Input Tax Credit (ITC) on the GST paid for these assets. This contributes to cost savings and improved operational efficiency.

Illustrative Example: A company purchases a vehicle intended for use in its delivery operations. The company can claim depreciation on the vehicle over several years and may also claim an ITC for the GST/VAT paid at the time of purchase.

Use of Capital Goods for Non-Business Purposes

When capital goods are used for non-business purposes, businesses lose out on tax advantages like depreciation and ITC claims. The cost benefits are limited, and tax authorities may require businesses to separate business and personal use for accurate reporting. This can lead to complications and potential penalties.

Illustrative Example: If the same vehicle is used for personal purposes by the owner or an employee, the business would not be eligible for depreciation deductions or the ITC on the purchase.

The impact of using capital goods for business versus non-business purposes directly influences the eligibility for tax deductions, credits, and liabilities. However, these benefits are not permanent, as certain conditions can trigger a reversal of the ITC on capital goods. Let’s explore the key scenarios in which such reversals are mandated.

Conditions for Reversal of ITC on Capital Goods

Understanding the conditions for ITC Reversal on capital goods is essential to maintaining compliance and avoiding unexpected financial setbacks. The ITC must be reversed under the following circumstances:

Non-Business or Exempt Use: If capital goods are used for personal purposes or in the supply of exempt goods/services, ITC must be reversed proportionately.

Non-Payment of Tax by Supplier: If the supplier does not remit tax within 180 days of the invoice date, the ITC must be reversed.

Depreciation Claimed: ITC must be reversed if depreciation is claimed on capital goods under the Income Tax Act.

Invoice or Goods Reversal: If goods are returned or an invoice is canceled, ITC should be reversed in the same tax period.

Business Transfer or Restructuring: In case of a business transfer or restructuring involving capital goods, ITC must be reversed for the transferred assets.

Non-Receipt of Goods or Mismatched Data: If goods or services are not received, or if there is a mismatch in supplier-reported and recipient-reported GST filings, ITC must be reversed.

GST Non-Compliance: Failure to comply with GST provisions or filing obligations can lead to ITC reversal.

Ensure your ITC claims on capital goods are seamless and compliant with Pazy‘s insights. Get started today to avoid ITC reversals and maximize your tax savings!

Once the conditions for reversal of ITC on capital goods are understood, it is equally important to comprehend how the sale or removal of capital goods affects the previously claimed ITC. The reversal process in these cases ensures that businesses adhere to GST regulations when capital goods are sold, removed, or otherwise no longer used for business purposes.

Read more: Understanding Reversal of Input Tax Credit under GST Rules

Reversal of ITC on Sale or Removal of Capital Goods

Reversal of ITC under GST allows businesses to claim credits only for eligible business activities, preventing misuse of the tax system. The reversal of ITC is calculated based on the following provisions:

Sale of Capital Goods

When capital goods are sold, the ITC claimed on the purchase of these goods must be reversed. The reversal will be calculated on a proportionate basis, depending on the remaining useful life of the asset. The formula for ITC reversal is as follows:

ITC Reversal=ITC Claimed × (Remaining LifeTotal Life)

This reversal applies if the capital goods are sold before the completion of their estimated useful life, as per the depreciation schedule.

Removal of Capital Goods

If capital goods are removed from the business for reasons other than sale (e.g., for personal use or donation), the ITC previously claimed on such goods must be reversed. As per Rule 40(2) of the CGST Act and SGST Rules 2017, the taxpayer must compute the amount by deducting 5% of the ITC for each quarter or from the date of the invoice for the specified capital goods. The reversal should be based on the original value of the capital goods and the period during which they were utilized for business purposes.

Time Period for Reversal

The reversal of ITC must occur in the tax period during which the capital goods are either sold or removed from the business.

Depreciation Claim

If depreciation is claimed on the capital goods under the Income Tax Act, the ITC initially claimed on those goods will be proportionately adjusted.

GST Implications on Sale or Transfer

The sale or transfer of capital goods may attract GST unless deemed an exempt or non-taxable supply. In such cases, the ITC reversal will apply even if the sale is subject to GST.

These provisions ensure the proper adjustment of ITC claimed on capital goods in cases where such goods are sold or removed. To further streamline this process, businesses can adopt tools like Pazy, which help optimize ITC rules for capital goods, ensuring accurate tax credit claims.

Optimize Input Tax Credit Rules for Capital Goods with Pazy

Pazy is an all-in-one automation platform that simplifies GST compliance for businesses. Automating invoice capture, GST validation, and 2A/2B reconciliation ensures accuracy and reduces manual effort. With real-time alerts and seamless integration, Pazy empowers businesses to stay compliant while optimizing tax benefits. It helps streamline the process of simplifying ITC rules for capital goods, ensuring your business maximizes its tax credit claims and minimizes the risk of errors or non-compliance.

Automated GST Reconciliation

Pazy’s automated GST reconciliation ensures that all transactions are matched accurately, eliminating manual errors and saving valuable time. It streamlines the entire process, making it faster and more efficient for businesses.

Real-Time Error Alerts

Pazy provides real-time alerts for any discrepancies or errors in GST filings, allowing businesses to address issues promptly. This proactive approach ensures compliance and minimizes the risk of costly mistakes during audits.

Accurate 2A/2B Reconciliation

With Pazy, businesses can automatically reconcile GST 2A and 2B data, ensuring accurate claims and minimizing discrepancies. This feature ensures that all input tax credits are correctly accounted for and compliant with tax regulations.Pazy simplifies ITC claims for SMBs, improving compliance and cash flow. Integrating with accounting tools simplifies processes for finance teams and enhances audit readiness. Industry-specific businesses and startups benefit from efficient ITC management, ensuring compliance and supporting growth.

Conclusion

Understanding and adhering to the ITC rules for capital goods is essential for businesses to remain compliant with GST regulations and avoid unnecessary tax liabilities. The input tax credit on capital goods ledger is created under these rules to ensure accurate tracking and reversal of ITC when capital goods are sold or removed. By ensuring proper calculations and timely reversals, businesses can optimize their tax credit claims.

Adopting tools like Pazy can further streamline this process, allowing businesses to efficiently manage their ITC claims, reduce errors, and maintain compliance. Ultimately, staying informed about these rules helps businesses maximize their tax benefits while minimizing risk.

Experience seamless GST compliance and optimize your Input Tax Credit management with Pazy. Schedule a Free Demo today and see how Pazy can streamline your business operations!

FAQs

1. Can ITC on capital goods be claimed immediately?

ITC on capital goods can be claimed in the same financial year when the goods are received, provided the GST returns are filed.

2. Can ITC be claimed on used or second-hand capital goods?

Yes, ITC can be claimed on used or second-hand capital goods, provided the conditions for claiming ITC under GST are met.

3. Can ITC on capital goods be availed in installments?

Yes, ITC on capital goods can be claimed in installments, with the total ITC being spread over a period of five years for most capital goods.

4. Is there any condition for claiming ITC on capital goods used for the construction of immovable property?

No, ITC cannot be claimed on capital goods used for the construction of immovable property, except in cases of construction of plant and machinery.

5. Can ITC be claimed on capital goods even if the GST invoice is not in the taxpayer’s name?

No, ITC can only be claimed if the GST invoice is in the name of the taxpayer claiming the credit.

OTHER BLOGS